Downtown Richmond Office (Click Our Homepage for More Info)

919 E Main St Suite 1000, Richmond, VA 23219

Phone:804-589-5989

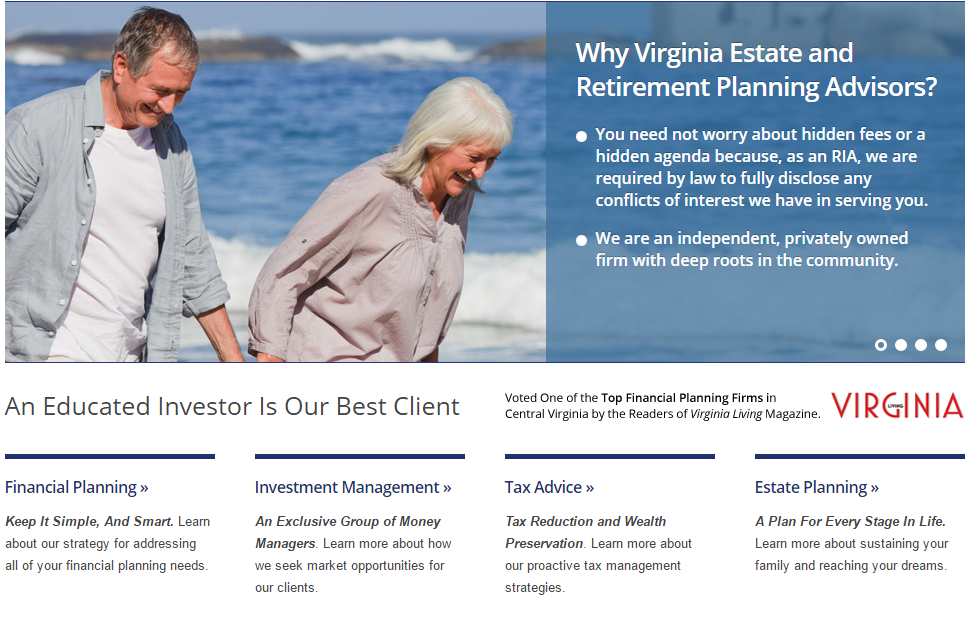

Why Choose Virginia Estate and Retirement Planning Advisors?

An Educated Investor Is Our Best Client

In today’s crowded financial landscape, you have countless options — from large Wall Street firms and insurance companies to robo-advisors and online brokers. So what sets one advisor apart?At Virginia Estate and Retirement Planning Advisors, Inc., we operate as a true fiduciary. This legal obligation means we are required to always put your best interests first. This is a meaningful difference from traditional brokers, and one that directly benefits our clients. Here’s how we’re different:

- We are a Registered Investment Advisor (RIA) — not a brokerage firm. We do not sell securities or earn commissions on stock or bond sales.

- Our only business is providing objective, personalized financial advice.

- As an RIA, we are legally required to disclose any potential conflicts of interest — so you can feel confident there are no hidden agendas or undisclosed fees.

- We are an independent, privately owned firm with strong local roots in Virginia.

- Because we grow primarily through client referrals rather than aggressive marketing, our success depends entirely on delivering exceptional service and results.

- Without pressure from corporate quotas or parent-company product lists, we have the freedom to recommend only the solutions that best fit your specific situation.

- Our approach centers on building a complete, long-term financial strategy tailored to your retirement, estate planning, and tax goals.

- You’ll work directly with experienced professionals who take the time to truly understand your needs and priorities.

This commitment to integrity and personalized service has earned us recognition in the community. Virginia Estate and Retirement Planning Advisors, Inc. has been voted “Best Financial Services Firm” by readers of the Richmond Times-Dispatch in nine of the last ten years. Our President and CEO, Thomas P. Marshall, has been named “Best Local Financial Planner” and has appeared as a trusted expert on ABC News Washington DC, NBC TV Roanoke, and CBS Virginia This Morning.

Financial Planner Richmond VA: How to Choose the Right Advisor for Your Wealth Goals

Finding the right financial planner in Richmond, VA can make a significant difference in reaching your money goals. The city has many options, from fee-only advisors to full-service wealth management firms. Each one offers different services and pricing models to meet your needs.

Richmond financial planners provide a wide range of services including retirement planning, tax strategies, investment management, and estate planning to help you build and protect your wealth. Many local firms work as fiduciaries, which means they must put your interests first. Some charge flat fees while others use different payment structures based on your situation.

When you start looking for a financial advisor, you need to understand what services matter most to you. Some planners focus on retirement strategies while others specialize in tax planning or helping business owners. The right choice depends on your specific financial situation and long-term goals.

Key Takeaways

- Richmond offers diverse financial planning options including fee-only advisors and fiduciary firms that prioritize your interests

- Financial planners in the area provide comprehensive services from retirement and tax planning to investment management and estate strategies

- Choosing the right advisor depends on understanding your specific needs, the fee structure, and the planner’s areas of expertise

Evaluating Top Financial Planners in Richmond, VA

Finding the right financial advisor in Richmond requires careful review of credentials, fee structures, and regulatory standards. Understanding these factors helps you select a professional who aligns with your financial goals and operates with your best interests in mind.

Key Criteria for Choosing an Advisor

When you search for a financial advisor, start by checking their credentials. A Certified Financial Planner (CFP) has completed specific education requirements and passed a comprehensive exam. This designation shows commitment to professional standards.

Look at the advisor’s experience level and areas of expertise. Some financial advisory firms focus on retirement planning, while others specialize in estate planning or tax strategies. Match their strengths to your needs.

Check how long the advisor has worked in Richmond. Local knowledge matters because Virginia has specific tax laws and estate planning rules. An advisor familiar with these details can provide better guidance.

Review client testimonials and ratings on platforms like YP and similar directories. Real feedback from other clients gives you insight into communication style and service quality. Pay attention to comments about responsiveness and personalized attention.

Fee Structures and Compensation Models

Fee-only financial planning means the advisor charges you directly for services with no commissions from product sales. This model reduces conflicts of interest because your advisor doesn’t profit from selling specific investments.

Some advisors charge an hourly rate, typically between $150 and $400 per hour. Others use a flat fee for specific services like creating a financial plan. Assets under management (AUM) fees usually range from 0.5% to 1.5% of your portfolio value annually.

Commission-based advisors earn money when you buy financial products they recommend. This fee structure can create potential conflicts since recommendations may benefit the advisor more than you. Ask direct questions about how your advisor gets paid.

Fee-based advisors combine both models, charging fees while also accepting commissions. Make sure you understand all costs before you commit. Request a clear breakdown in writing that lists every charge you might encounter.

Regulation and Fiduciary Responsibility

A fiduciary financial advisor must legally put your interests first. This standard requires them to recommend strategies that benefit you, even if it means lower compensation for them. Not all financial advisors operate as fiduciaries.

Check if your advisor is registered with the Securities and Exchange Commission (SEC) or the Virginia State Corporation Commission. You can verify credentials and review any disciplinary history through FINRA’s BrokerCheck database.

Investment advisor representatives must act as fiduciaries under the Investment Advisers Act. Broker-dealers follow a less strict “suitability” standard. Know which category your advisor falls under because it affects their legal obligations to you.

Ask potential advisors directly if they commit to fiduciary duty for all services. Get this commitment in writing as part of your service agreement.

Local Recognition and Industry Awards

Richmond has several recognized financial planning professionals. Best financial advisors lists from organizations like Expertise.com evaluate firms based on reputation, client reviews, and professional achievements.

Industry recognition provides useful signals about quality and reliability. Awards show that peers and industry experts respect the advisor’s work. However, don’t rely solely on these honors when making your decision.

Some directories list 46 firms and over 1,300 advisors in the Richmond area. This large number means you need additional filtering criteria beyond awards. Combine recognition with your own research on credentials and services.

When you find a financial advisor through ranking sites, verify their information independently. Contact the firm directly to confirm current services, fees, and availability. Rankings provide a starting point, not a final answer.

Comprehensive Services Offered by Richmond Financial Planners

Richmond financial planners provide integrated solutions that address multiple aspects of your financial life, from managing investment portfolios to protecting your assets through insurance analysis. These professionals structure their services around your specific goals and circumstances.

Personalized Wealth Management

Wealth management in Richmond goes beyond basic investment advice. Your wealth advisor examines your complete financial picture, including income sources, existing assets, debt obligations, and long-term objectives.

Financial planners coordinate various elements of your finances into one cohesive strategy. They work with you to identify priorities, whether that’s funding education costs, purchasing property, or building generational wealth.

Many Richmond firms operate as fiduciaries, which means they must act in your best interest. This structure ensures recommendations align with your needs rather than commission-based products. Your advisor tracks progress regularly and adjusts strategies as your life circumstances change.

Investment Management and Asset Allocation

Investment management focuses on building and maintaining your investment portfolio according to your risk tolerance and timeline. Richmond advisors handle the selection, monitoring, and rebalancing of your assets under management.

Asset allocation divides your investments across different categories like stocks, bonds, and alternative investments. Your advisor determines the right mix based on factors including your age, income needs, and comfort with market fluctuations.

Portfolio management involves ongoing oversight of your holdings. Advisors make tactical adjustments when markets shift or when your personal situation changes. They also handle tax-efficient placement of investments across different account types.

Financial Planning and Portfolio Management

Financial planning services in Richmond create structured roadmaps for your money. Planners analyze your current situation, project future needs, and develop actionable steps to bridge the gap between where you are and where you want to be.

Retirement planning forms a core component of these services. Your planner calculates how much you need to save, recommends contribution levels, and projects income sources during retirement years.

Estate planning coordination helps ensure your assets transfer according to your wishes. Tax optimization strategies work to minimize your liability across income, capital gains, and estate taxes. These elements integrate with your investment portfolio management to create a complete financial framework.

Risk and Insurance Analysis

Insurance analysis identifies gaps in your current coverage and matches protection to your actual needs. Your advisor reviews policies from various insurance companies to find appropriate coverage levels at competitive rates.

Risk management evaluates potential threats to your financial security. This includes assessing liability exposure, income loss scenarios, and long-term care needs. Insurance planning then addresses these risks through term life, disability, umbrella policies, and other products.

Richmond planners also examine business insurance if you own a company. They verify that your personal and professional assets receive adequate protection without paying for unnecessary coverage.

Retirement and Estate Planning Solutions

Financial planners in Richmond, VA help you structure retirement accounts, generate reliable income streams, optimize Social Security timing, and protect assets for future generations through coordinated estate strategies.

Retirement Plan Design

Your retirement plan design starts with selecting the right account types for your situation. Common options include 401(k)s, IRAs, Roth IRAs, and SEP IRAs for self-employed individuals. Each account has different contribution limits, tax treatments, and withdrawal rules.

Financial planners evaluate your current income, tax bracket, and employer benefits to determine which accounts maximize your savings potential. They also review beneficiary designations and ensure your retirement accounts align with your overall financial goals.

For business owners, retirement plan design involves choosing between SIMPLE IRAs, solo 401(k)s, or defined benefit plans. The right structure depends on your business size, employee count, and how much you want to contribute annually.

Retirement Income Planning Strategies

Creating sustainable retirement income requires coordinating multiple income sources. You might draw from Social Security, pensions, retirement accounts, investment portfolios, and rental properties. The sequence and timing of these withdrawals significantly impact how long your money lasts.

Tax-efficient withdrawal strategies help you minimize your tax burden during retirement. Financial planners often recommend withdrawing from taxable accounts first, then tax-deferred accounts, and finally Roth accounts. This approach manages your tax bracket year by year.

Required minimum distributions (RMDs) from traditional IRAs and 401(k)s begin at age 73. Planning for these mandatory withdrawals prevents unexpected tax bills and helps you maintain control over your income streams.

Maximizing Social Security Benefits

Your Social Security claiming age affects your monthly benefit amount for life. Claiming at age 62 reduces your benefit by up to 30%, while delaying until age 70 increases it by 8% per year after full retirement age.

Claiming strategies to consider:

- File and suspend – No longer available but grandfathered for some

- Spousal benefits – Claim up to 50% of your spouse’s benefit

- Survivor benefits – Widows can switch between benefits

- Earnings test awareness – Working while collecting before full retirement age reduces benefits

Coordination between spouses creates opportunities to maximize household benefits. One spouse might claim early while the other delays, balancing immediate income needs with long-term benefit growth.

Estate Planning Essentials

Estate planning protects your assets and ensures they transfer according to your wishes. Basic documents include a will, durable power of attorney, healthcare power of attorney, and living will. These documents prevent court intervention and family disputes.

Trusts offer additional control over asset distribution. Revocable living trusts avoid probate, while irrevocable trusts can reduce estate taxes and protect assets from creditors. The trust structure you need depends on your estate size and family circumstances.

Beneficiary designations on retirement accounts and life insurance policies override your will. Review these designations every few years, especially after major life events like marriage, divorce, or the birth of children. Estate planning also involves tax planning strategies to minimize the burden on your heirs.

Tax Strategies and Preparation

Financial advisors in Richmond, VA help you reduce your tax burden through smart planning throughout the year and accurate preparation during tax season. The right tax strategies can protect more of your wealth while ensuring you meet all your obligations to the IRS and state authorities.

Year-Round Tax Planning

Tax planning works best when you address it continuously rather than just before the April deadline. Your financial advisor reviews your income sources, deductions, and credits each quarter to identify opportunities for tax savings. This approach lets you adjust your withholdings, make estimated tax payments, and time income or expenses strategically.

Many Richmond advisors work with you to maximize contributions to tax-deferred retirement accounts like 401(k)s and IRAs. These moves lower your taxable income for the current year while building your retirement savings. Your advisor also monitors changes in tax laws that might affect your situation and recommends adjustments to your strategy as needed.

Tax Preparation Services

Richmond financial planners often provide tax preparation or partner with tax professionals to handle your annual filing. They ensure your returns are accurate and submitted on time for both federal and Virginia state requirements. Professional preparation reduces your risk of errors that could trigger audits or penalties.

Your tax preparer gathers documentation for all income sources, including wages, investment gains, rental income, and business earnings. They identify every deduction and credit you qualify for based on your specific circumstances. Fee-only advisors in Richmond typically charge transparent rates for these services rather than commissions.

The preparation process includes reviewing your previous year’s return to catch any missed opportunities or errors. Your advisor can also represent you if questions arise from tax authorities.

Tax-Efficient Investment Strategies

Your investment choices directly impact your annual tax bill. Financial advisors in Richmond structure your portfolio to minimize taxes while pursuing your growth objectives. Tax-efficient strategies include holding investments for more than one year to qualify for lower long-term capital gains rates instead of higher short-term rates.

Your advisor may recommend:

- Municipal bonds that generate tax-free interest income

- Index funds with lower turnover that create fewer taxable events

- Tax-loss harvesting to offset gains with strategic losses

- Asset location that places tax-inefficient investments in retirement accounts

These approaches help you keep more of your investment returns each year without sacrificing your financial goals.

Charitable Giving and Legacy Tax Planning

Strategic charitable giving reduces your taxable estate while supporting causes you care about. Your Richmond financial advisor structures donations to maximize tax benefits through methods like donor-advised funds or direct gifts of appreciated securities. Giving stock instead of cash lets you avoid capital gains taxes while still claiming the full fair-market-value deduction.

Estate planning integrates with your tax strategy to minimize the burden on your beneficiaries. Your advisor helps you use gift tax exemptions effectively and structure trusts that protect assets from excessive taxation. They coordinate with estate attorneys to ensure your legacy plan aligns with current tax laws at both federal and state levels.

Specialized Planning for High Net Worth Individuals

High net worth individuals require more complex financial strategies that go beyond basic investment management. Private wealth management addresses unique challenges like tax optimization, estate planning, and coordinating multiple asset types to protect and grow substantial wealth.

Wealth Preservation Techniques

Protecting your accumulated wealth requires strategic planning across multiple financial areas. Financial planners use diversification strategies that spread assets under management across different investment classes to reduce risk exposure. Tax-efficient investment structures help you keep more of your returns by minimizing tax liabilities on income, capital gains, and dividends.

Asset protection strategies shield your wealth from potential creditors and legal claims. These include establishing trusts, creating legal entities for business holdings, and structuring ownership to limit personal liability. Your advisor will evaluate insurance coverage gaps and recommend policies that protect against significant financial losses.

Private wealth management teams coordinate with tax professionals and attorneys to create comprehensive protection plans. They monitor your portfolio regularly and adjust strategies as tax laws change or your financial situation evolves.

Philanthropy and Charitable Trusts

Charitable giving strategies let you support causes you care about while gaining tax benefits. Donor-advised funds allow you to contribute assets, receive an immediate tax deduction, and recommend grants to charities over time. This approach gives you flexibility in timing your donations while maximizing tax savings.

Charitable remainder trusts provide income to you or your beneficiaries for a set period, with remaining assets going to charity. Private foundations offer more control over charitable activities but require additional administrative work and compliance.

Financial advisors help structure your charitable giving to align with your values and financial goals. They calculate the tax implications of different donation methods and coordinate with your estate planning to include philanthropic objectives.

Multi-Generational Wealth Transfer

Estate planning for high net worth families involves moving assets to future generations while minimizing estate taxes and protecting family wealth. Irrevocable life insurance trusts remove life insurance proceeds from your taxable estate while providing liquidity for your heirs.

Family limited partnerships and limited liability companies allow you to transfer business interests to children or grandchildren at reduced tax values. Grantor retained annuity trusts let you pass appreciating assets to beneficiaries while retaining income streams during your lifetime.

Your advisor coordinates with estate attorneys to update documents as laws change and your family situation evolves. They help establish governance structures that prepare the next generation to manage inherited wealth responsibly. Regular family meetings ensure everyone understands the wealth transfer plan and their future responsibilities.

Frequently Asked Questions

Finding the right financial planner requires understanding advisor types, fee structures, credentials, and how to evaluate their trustworthiness. Richmond has 46 financial advisory firms and 1,320 financial advisors to choose from, making it important to know what questions to ask and what factors matter most.

How do I choose a trustworthy financial advisor in my area?

Start by verifying the advisor’s credentials and checking their background through FINRA’s BrokerCheck or the SEC’s Investment Adviser Public Disclosure database. These tools show you licensing information, employment history, and any disciplinary actions.

Look for advisors who specialize in your specific needs, whether that’s retirement planning, wealth management, or tax strategies. Interview at least three advisors before making a decision.

Ask each advisor how they get paid, who their typical clients are, and what services they provide. Trust your instincts during these conversations—you should feel comfortable asking questions and receiving clear answers.

What is the difference between a fiduciary advisor and a non-fiduciary advisor?

A fiduciary advisor must legally put your interests first in all situations. They cannot recommend products or strategies that benefit them more than you, even if those products are suitable for your situation.

Non-fiduciary advisors work under a suitability standard. This means they only need to recommend products that are appropriate for you, not necessarily the best options available.

Fiduciary advisors must disclose all conflicts of interest in writing. Non-fiduciary advisors might earn commissions from products they sell to you, which can create incentives to recommend certain investments.

How do fee-only financial planners charge, and what services are typically included?

Fee-only planners charge in three main ways: a percentage of assets under management, flat fees, or hourly rates. In Richmond, the median advisory fee is 1.15% of assets under management.

Assets under management fees typically range from 0.5% to 2% annually. This model works well if you have a substantial investment portfolio and want ongoing management.

Flat fee arrangements might cost $2,000 to $7,500 per year depending on your complexity. Hourly rates usually fall between $150 and $400 per hour for specific advice or one-time planning.

Services often include investment management, retirement planning, tax planning, estate planning guidance, and regular portfolio reviews. Some planners also offer budgeting help and insurance analysis.

What questions should I ask during an initial consultation with a financial planner?

Ask about their qualifications first. Find out what certifications they hold, such as CFP (Certified Financial Planner), CPA, or CFA.

Request details about their fee structure and get everything in writing. Ask how they make money and whether they receive commissions from any products they recommend.

Learn about their experience with clients in similar situations to yours. Ask how often you’ll meet, how they communicate between meetings, and who will handle your account day-to-day.

Find out their investment philosophy and approach to risk management. Ask about their typical client profile and how many clients they currently serve.

How can I verify an advisor’s credentials, licensing, and disciplinary history?

Use FINRA’s BrokerCheck at brokercheck.finra.org to look up brokers and brokerage firms. This free database shows employment history, exams passed, licenses held, and any complaints or disciplinary actions.

Check the SEC’s Investment Adviser Public Disclosure system at adviserinfo.sec.gov for registered investment advisors. You can view their Form ADV, which details their services, fees, conflicts of interest, and disciplinary history.

Visit the CFP Board’s website at cfp.net/verify-a-cfp-professional to confirm CFP certification status. The site shows whether someone is currently certified and if they’ve faced any disciplinary actions.

Your state securities regulator also maintains records of advisors operating in Virginia. Contact them if you can’t find information through the national databases.

What should I look for in client reviews and ratings when comparing financial advisors?

Read reviews on multiple platforms, not just the advisor’s own website. Check Google, Yelp, and industry-specific sites for a broader perspective.

Pay attention to comments about communication style and responsiveness. Good advisors should return calls promptly and explain complex topics in ways you understand.

Look for patterns in reviews rather than focusing on single complaints. Multiple mentions of the same issue—whether positive or negative—carry more weight than isolated incidents.

Notice how advisors respond to negative reviews. Professional responses that address concerns show accountability and customer service commitment.

Be skeptical of profiles with only five-star reviews or very few reviews overall. A mix of ratings with detailed explanations often indicates more authentic feedback.